Properly, it's inventory commerce … – The Healthcare Weblog

By Matthew Holt

These days there was a lot dialogue about whether or not digital well being is a legit place for danger capital. There have been many big failures, however only a few outstanding successes (and positively not but “largest corporations on the planet”), whereas some actual giants (Walmart/Walgreens/Amazon) have arrived after which got here out of well being care.

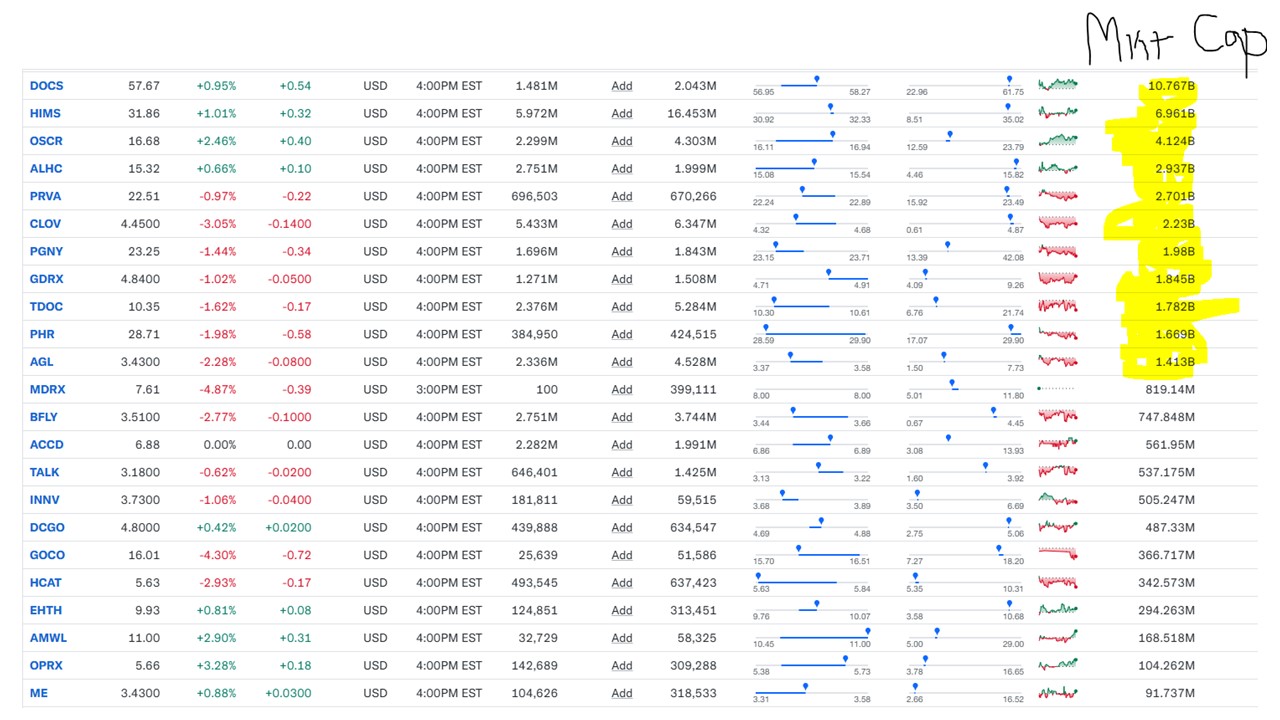

I don't must inform you once more that almost all listed digital well being corporations act on cash on the greenback to their first scores. However I'll do it. Take a look at that graph beneath.

Even Doximity – who prints cash (45% internet margins!) – acts properly beneath the submit -IIPO Excessive. My fast overview is that there usually are not many listed corporations at Unicorn standing. With actually solely doximity, HIMS and Oscar are very profitable. (We are able to have a separate argument about whether or not Tempus and Waystar are “digital well being”). And there are numerous, many who’re good of the value they’re on. All at a time when the common inventory market hits report heights.

That makes it attention-grabbing to say that Outline Ventures simply got here out with a report that stated that generally digital well being has executed properly as a enterprise funding and that it could in all probability do higher, quick.

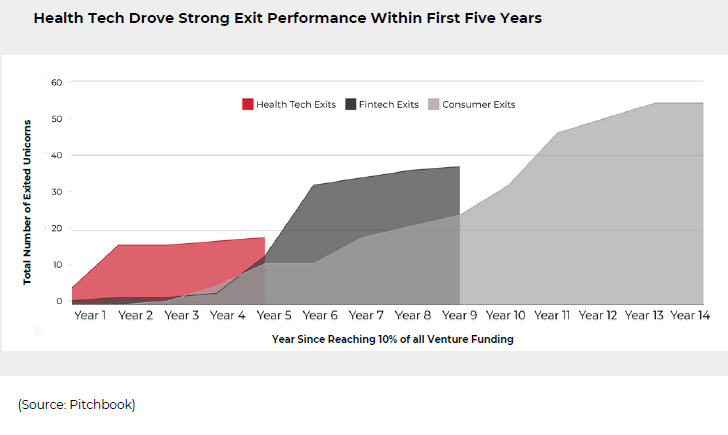

The report will not be that lengthy and is value studying, however their fundamental argument compares digital well being investments with individuals in fintech and shopper tech. In essence, digital well being took for much longer to get 10% of the whole enterprise investments than fintech or shopper expertise, however it got here after 2020. Now greater than 10% of all VC supported unicorns are well being expertise corporations. Sure, there was a reduce in 2022-3, however the funding of well being expertise fell fewer Then different sectors in 2022-3 and is in precept again in 2024.

The prediction prediction of defining is attention-grabbing (it’s the graph beneath). Defines stealing that it took 4-5 years after the sectors of fintech and shopper tech 10% of VC {Dollars} have been for them to pump out outputs and IPOs. There at the moment are 30-50 every in these sectors, however Well being Tech ran for 18 outputs that already within the first 5 years after reaching 10% of VC {dollars}, and people outputs have been on common double the fintech/ Client Tech outputs. (Though to be trustworthy, the outputs of well being expertise have been when the market was increased after 2020)

The truth is, their evaluation is that Capital Returned was round 10x investments. You would say, however hey Matthew didn't simply present me a graph that almost all of these 18 corporations have been canine for the general public market? And you’d be proper.

If we have a look at the 18 corporations that outline exams, they don’t actually match the record of 11 unicorns that I’ve on my card earlier, however generally they didn’t do properly in the long run.

Some have perished (Science 37 & NuueHealth bought for components), some have been bought for actual cash, in the event that they have been a lot lower than they’d ever traded (one medical was $ 50 per share at a sure level however purchased for $ 18, However that was $ 3.9 billion together with money owed, award was simply bought by Transcarent for round $ 600 million), whereas most have slowly been rejected to good lower than IPO value (Amwell, Talkspace, Well being Catalyst and all of the bits at the moment in TELADOC, together with Livongo & Intouch).

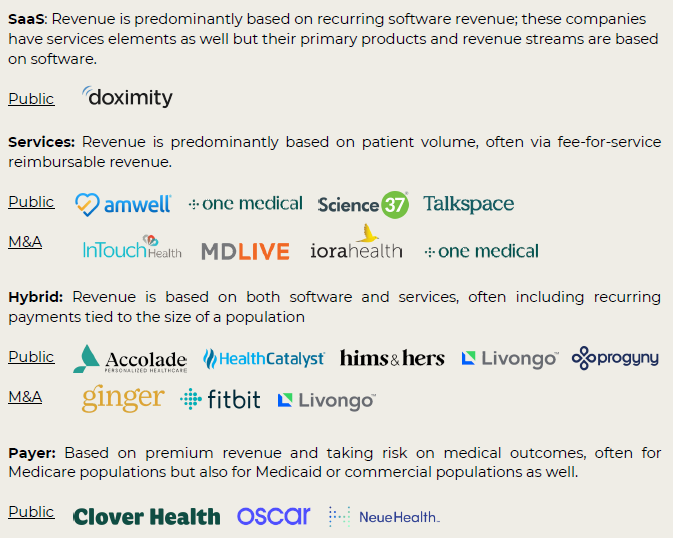

However Outline in contrast the efficiency of these public corporations with another unprofitable public corporations within the early stage and noticed that these corporations that outlined as “companies” and “payers” did worse, however “hybrid” and “SaaS” did higher than Different expertise corporations.

(By the way in which, it’s fairly superb that somebody has compiled an index of loss to make public expertise corporations, however apparently Morgan Stanley! It’s referred to as MSPTX, though my googling can't discover it!)

Outline additionally means that the next set of digital well being corporations which can be made public or will do that quicker and at a better worth via mergers and acquisitions. Typically, it is because “Part Components Tech” is extra simply that can be purchased from the shelf, with AI the plain “element” instance. That’s the reason these corporations will scales quicker and AI will speed up that. Right here is their record, together with one service firm, Carebridge, which already had a superb exit.

However I’m nonetheless very involved that these corporations can not obtain a smart appreciation primarily based on what they’ve elevated. Let's examine them with the favourite of what defines “Wave 1” of IPOs for well being expertise. Livongo raised $ 237 million for his IPO. Okay that's not a rooster feed, however it was appreciated beneath $ 1 billion for the IPO and about $ 4 billion shortly after the IPO. 3 months later, it once more acted nearer to $ 2 billion after which began his pandemic pushed enhance in a market capitalization of $ 20 billion and the well-known $ 19 billion merger with Teladoc.

$ 237 million could sound like quite a bit for the whole capital, however Innovacer has raised $ 675 million, Lyra & Hinge Well being nearly $ 1 billion every, together with the well being parts have “solely” raised $ 500 million and the devoted well being has extra Then collected $ 2.25 billion. So these corporations should exit on multi-billion greenback scores to do one thing like that in comparison with the success of Livonogo, after which public market traders (or their buying corporations within the case of mergers and takeovers) will anticipate that they develop from there. Given the efficiency of corporations within the sector now, and that there are nonetheless many comparable corporations which can be value a lot much less on the general public market, these personal corporations have quite a few monumental performances, otherwise you would think about that they may disappoint their traders .

So how can the definition of the declare that the primary wave of corporations has invested 10 instances the capital?

I believe that’s comparatively easy.

Lots of these corporations have been linked or have been taken over at a value that’s good above the place they ended up. However in case you have been an investor at an early stage who may promote within the IPO or shortly thereafter, you may need retoured that.

Possibly when you’ve got invested within the second wave early sufficient, you may see that return too. However so a lot of these corporations have raised a lot cash in such a excessive ranking within the Halcyon days of 2021 & early 2022 (to not point out on the finish of 2024 and early 2025) that it’s tough to have these ranges of returns for many Traders to see. And if you’re after all a public market investor who buys within the foaming interval after IPO, the prospect that you can be led to a pigs are certainly very excessive.

However if you’re a VC and you should buy low cost sufficient, you may obtain nice returns. So long as you do your shares fastidiously and are fortunate!