KFF follow-up survey of market enrollees: After the top of enhanced credit score, half of market enrollees now say prices are a lot increased, most anticipate to chop again on primary family bills to supply protection

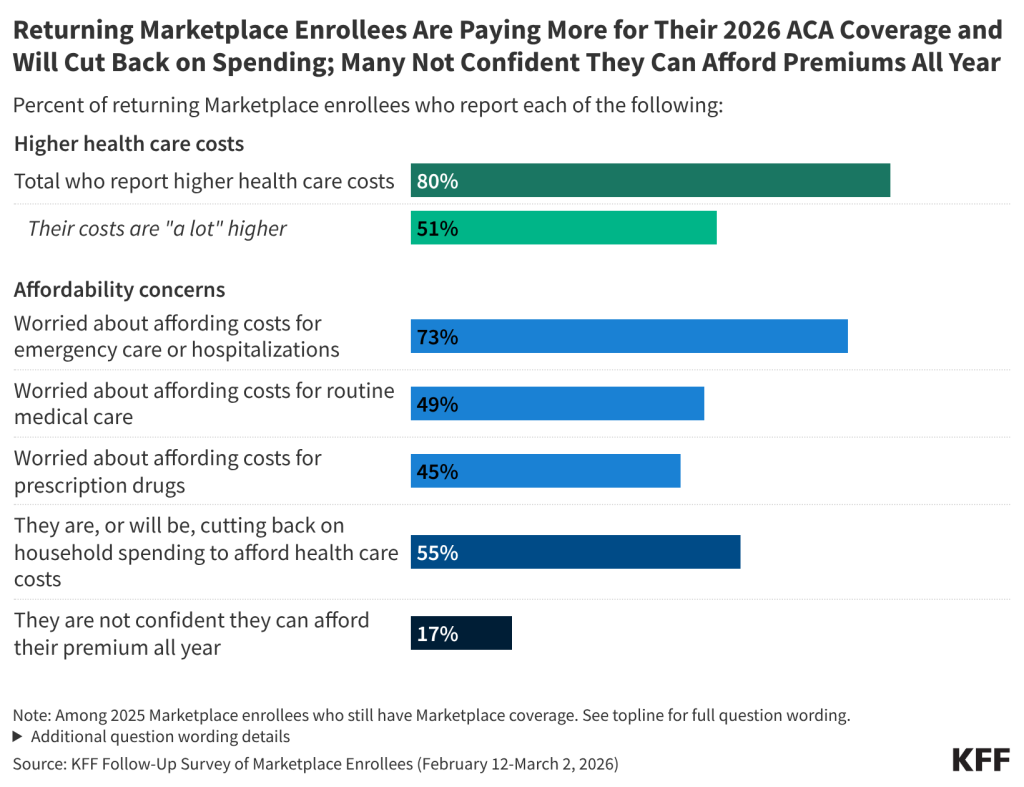

Following the expiration of enhanced premium tax credit for these on Reasonably priced Care Act (ACA) Market plans, a brand new KFF follow-up survey of the identical Market enrollees surveyed in 2025 finds that KFF half (51%) of returning enrollees say their well being care prices are “lots increased” this 12 months than final 12 months, together with 4 in 10 who particularly say their premiums are “lots increased.” General, a big majority (80%) of those enrollees say their well being care prices, together with premiums, deductibles, co-pays or coinsurance, are increased.

This new survey, carried out a couple of month after open enrollment led to most states and earlier than the grace interval for making funds ended for a lot of enrollees, once more interviewed Market individuals who shared their expectations about their protection choices late final 12 months. It additionally finds that almost one in six (17%) returning ACA Market enrollees say they’re not sure they may be capable of pay their premiums this 12 months. For many who have retained the identical Market plans, the expiration of the ACA’s enhanced premium tax credit in 2025 is estimated to greater than double annual premium funds on common this 12 months.

Responding to rising healthcare prices

Amongst those that have re-enrolled in an ACA Market plan, a majority (55%) say they’ve reduce or plan to chop again on meals or different primary family bills to pay for his or her well being care prices. The affect is even larger for folks with continual well being situations; greater than six in ten (62%) of them say they’re or will reduce on meals and different primary wants.

Market individuals are additionally involved about their capability to pay for each routine and sudden medical bills. About three-in-four (73%) returning Market individuals say they’re “very involved” or “considerably involved” about having the ability to pay for emergency care or hospital admissions, whereas about half fear about the price of routine medical visits (49%) or pharmaceuticals (45%).

“The affect on Market individuals that we see on this follow-up survey will doubtless worsen as folks wrestle to make funds and the grace interval expires for a lot of,” mentioned KFF President and CEO Drew Altman.

For some, rising prices have already pressured them to make troublesome decisions. About one in ten (9%) Market enrollees have dropped their ACA protection and are actually uninsured, whereas one other almost three in ten (28%) have modified their Market plan. When requested why they determined to drop or change their protection, most cited prices.

A 63-year-old man in California describes why he’s now uninsured:

“The tip of the ACA subsidies brought about an enormous improve in premiums, the price of which I couldn’t afford.”

A 56-year-old man in Texas explains why he switched to a distinct Market plan:

“Earnings exceeded the subsidy restrict, forcing us to pay the complete value, so we switched to a bronze plan from a gold plan. Even when we try this, our premiums can be 3 times what they might be in 2025, with decrease plan options and the next deductible.”

General, seven-in-ten (69%) of those that had ACA Market protection in 2025 re-enrolled in a plan by way of the Market, whereas others certified for various kinds of medical insurance, both by way of an employer (5%), or by way of Medicare (4%) or Medicaid (7%). A small share (5%) bought well being plans exterior of the ACA Market, which usually affords much less complete protection and fewer shopper protections than Market plans. Even in years with few coverage modifications, shifts between Market plans or to different sorts of protection are widespread and infrequently comply with modifications in employment, revenue, age, and different residing situations.

Waiting for the midterm elections

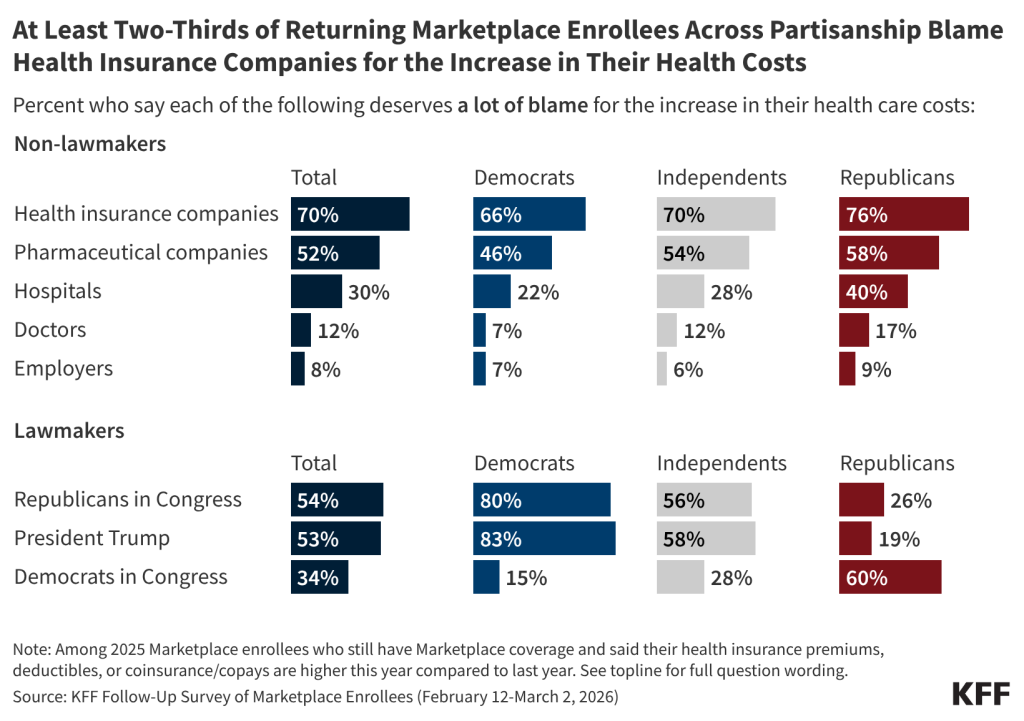

Amongst returning Market individuals who noticed increased healthcare prices, seven-in-ten (70%) blame well being insurers “lots” for his or her increased prices, and at the very least half blame Republicans in Congress (54%), President Trump (53%) or pharmaceutical corporations (52%) “lots.” Whereas a majority of partisans place “lots” of blame on opposing get together lawmakers, independents with Market reporting usually tend to say that Republicans in Congress (56%) and President Trump (58%) deserve “lots” of blame than Democrats in Congress (28%).

Three-quarters of those that had protection by way of Market in 2025 and are registered to vote say well being care prices will affect their choice to vote (73%) and which get together candidate they may assist (74%). Democrats are greater than twice as doubtless than Republicans to say this may have a significant affect on their choice to vote (67% vs. 27%) and which candidate to assist (70% vs. 30%). Amongst unbiased voters, nearly half say the difficulty may have a significant affect on their choice to vote (47%) and which candidate they may assist (44%).

Designed and analyzed by public opinion researchers at KFF, this survey, which builds on a 2025 survey of ACA Market enrollees, re-interviewed greater than 80% of the unique pattern to see how they’re dealing with modifications within the ACA Market. The survey was carried out from February 12 to March 2, 2026, on-line and by phone, in English and Spanish, amongst a nationally consultant pattern of 1,117 U.S. adults who had protection on the ACA Market in 2025 and accomplished the primary KFF survey. The margin of sampling error is plus or minus 4 share factors for all the pattern. For outcomes primarily based on different subgroups, the margin of sampling error could also be bigger.